Comparativas

Do Contractors Charge Sales Tax? A US Construction Guide (2026)

A cautious, contractor-friendly guide to sales tax in the US: when materials, labor, or full jobs may be taxable, how to show tax in an estimate, and what to verify locally.

Sales tax is one of the easiest parts of an estimate to get wrong because the answer is not the same everywhere. In some states, materials are taxable but labor is not. In others, both may be taxable. In others, the contractor may owe tax on the full job or on the materials purchased for the work. That is why this guide stays cautious: always verify the rule for the exact state, city, and type of work before you send the estimate.

This guide is informational only and does not replace advice from a CPA, tax advisor, or state tax authority.

Why sales tax varies so much

- Some states tax materials but not labor

- Some states tax labor for certain jobs and not others

- Some states treat construction contractors differently from retail sellers

- Local city or county rules may add another layer

- Special jobs can have special tax treatment

The safest mindset is to assume the rules are local, not universal. If you work in more than one state, keep a simple checklist by state so your estimating workflow stays consistent instead of relying on memory.

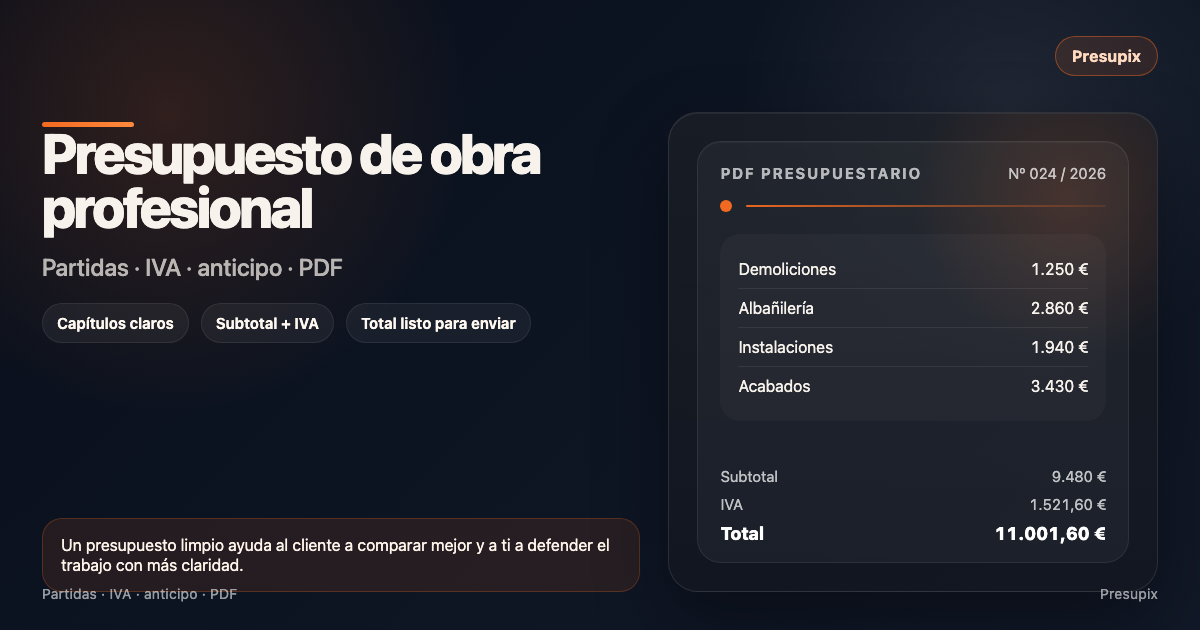

How to show tax clearly in an estimate

| Line | Example | Why it helps |

|---|---|---|

| Labor | $2,400 | Makes the estimate easier to read |

| Materials | $1,150 | Shows what can be taxed separately |

| Sales tax | Varies by state | Keeps the tax treatment visible |

| Permit / fee | $125 | Avoids hidden extras |

| Total | $3,675+ | Final amount depends on local rules |

If the tax treatment is not clear, do not guess in a way that sounds official. Use a clear note instead: sales tax applied according to local rules, to be confirmed before invoicing. That keeps the estimate honest and avoids promising something you have not verified.

Common tax scenarios contractors run into

- Painting or remodeling in a home where only materials are taxable

- Electrical or plumbing jobs where parts are taxable and labor is not

- Full remodels where tax applies to the full contract value in some states

- Supplied materials versus customer-supplied materials

- Emergency service jobs with different documentation requirements

The estimate should make the tax assumption visible enough that your customer understands the final number may change if the tax authority treats the job differently. That is much better than hiding tax inside a round total and having to explain it later.

A simple estimate structure when sales tax applies

- Scope of work

- Labor subtotal

- Materials subtotal

- Sales tax note or line

- Total before and after tax

- Payment terms and deposit

If you send a client-ready PDF, the customer can see the labor, materials, and tax treatment in one document instead of trying to piece it together from text messages or screenshots. That makes your estimate feel more professional and reduces back-and-forth.

What to verify before you finalize the estimate

- State sales tax rule for contractor work

- Whether labor, materials, or both are taxable

- Whether permits or disposal fees are taxable

- Whether your city or county adds a local rate

- Whether the customer is a homeowner, business, or public entity

Frequently asked questions

Do contractors always charge sales tax?

No. The answer depends on the state, the type of job, and whether the charge is for labor, materials, or both.

Should I show sales tax as a separate line?

Yes, if the rules for your area require it or if showing it separately makes the estimate easier for the client to understand.

Can I rely on this guide instead of tax advice?

No. This guide is informational only and does not replace advice from a CPA, tax advisor, or state tax authority.